Property investors have taken a further hit with several lenders making it more difficult to obtain finance for buy-to-let. This comes after a series of bad news including Stamp Duty rises and tax relief cuts on mortgage interest. However, if property prices fall faster than rent, could this work in favour for landlords and buy-to-let mortgages.

This does not constitute advice and advice should be sought in all instances before acting on it.

Your property may be at risk should you be unable to maintain any agreed mortgage payments over the term agreed.

Tighter lending policy for buy-to-let

TSB are the latest lender to tighten their lending policy for buy-to-let mortgages. This follows Nationwide and Barclays earlier this year. These lenders have decreased the amount they will lend to a landlord in comparison to their anticipated rental income.

Lenders are taking measures in line with a Bank of England (BoE) consultation, the outcome of which will be announced later this summer. The consultation could result in tighter regulations for lenders regarding buy-to-let mortgage applications, forcing them to also take into account the wider costs of a landlord, even including tax.

Landlords are losing money

All-in-all landlords are having to, or will need to, either increase their rental price to cover additional costs, or take less profit. Some may also struggle to obtain finance for new buy-to-lets or, they could get stuck on a buy-to-let mortgage with a high interest rate, as they won’t meet new lending criteria to remortgage.

This is similar to what is also happening with some residential mortgages, only the government “have it in” for property investment at the moment, so everything is an uphill climb.

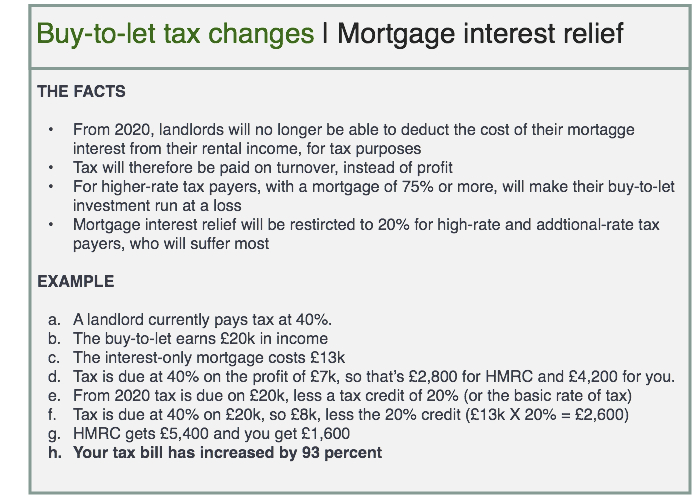

Experts calculate that for a landlord paying tax at higher-rate, they will need to cover their rental income by over 150 percent, with the new changes to mortgage interest alone. This could be even more if mortgage lending policy changes too.

“Mathematically speaking, it makes sense for higher-rate taxpaying landlords to need rental cover at 156pc, and additional-rate taxpaying landlords at 167pc.” Mortgages for Business

How Brexit could help landlords with short-term goals

The market is predicting that house prices will take a tumble after Brexit, with the country preparing for another recession.

If house prices do ease-off and, if rental yields remain the same, this could offer some temporary relief for property investors in terms of obtaining buy-to-let finance.

It isn’t such good news for the existing property portfolio, however, given time, this will hopefully bounce back.

What it may do though is bring a reduction in the mortgage payment, compared to the rental income, allowing the new mortgage application hurdles to be jumped.

As there is much uncertainty and change at the moment, it is important to seek advice from professionals that can help you make the right decisions and get the timing right.

Need a buy-to-let mortgage. Speak to Chris

If you need to discuss a new or existing buy-to-let mortgage, speak to Chris, our specialist mortgage broker. He can discuss the best rates and a plan of action.

Tel: 01403 780 770

Follow us on Twitter and LinkedIn for regular financial and mortgage updates

?

If you found this article interesting, why not share it

If you found this article interesting, why not share it

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful. You can adjust your preferences here. Please see our privacy policy for more information relating to GDPR.

All questions, comments and requests regarding this Cookies Policy should be addressed to [email protected] write to Us at 1 Market Square, Horsham, West Sussex, RH12 1EU.

Or alternatively please contact our Compliance Director at Best Practice IFA Group Ltd, Broadlands Business Campus, Langhurst Wood Rd, Horsham, RH12 4QP, telephone number 01403 334455, or via email at [email protected]

Strictly Necessary Cookies

These cookies are necessary for the website to function and cannot be switched off in our systems. They are usually only set in response to actions made by you which amount to a request for services, such as setting your privacy preferences, logging in or filling in forms. You can set your browser to block or alert you about these cookies, but some parts of the site may not work then.

Cookies used:

moove_gdpr_popup - Stores user preferences in regards to cookie settings

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.

3rd Party Cookies

This website uses Google Analytics and other marketing cookies to collect anonymous information such as the number of visitors to the site, and the most popular pages.

Keeping this cookie enabled helps us to improve our website.

Cookies used:

Google tag manager

Please enable Strictly Necessary Cookies first so that we can save your preferences!

Tel: 01403 780 770

Tel: 01403 780 770