In recent months and years, home owners, landlords and first time buyers in the UK have been racing to the banks to secure fixed-rate mortgages as if it may be their last chance. In many cases securing a fixed rate mortgage whilst the rates are low can be seen as advantageous. However, for others it may not be the best decision.

Here are 5 things to consider before committing to a fixed-rate mortgage.

1 – Interest rates may not even rise

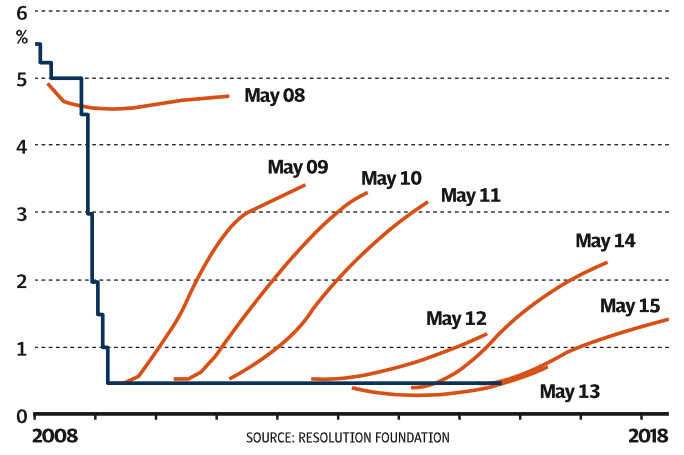

This chart by Resolution Foundation plots the rate predictions versus actual performance. The orange lines represent how economists viewed the rate fluctuations since 2008, compared to the black line which represents a very different reality.

Rate rises are predicted for early 2016 according to the latest news and views from the experts. However, as this graph proves, they don’t always get it right.

Consider this if you are opting for a fixed-rate mortgage based purely on pressure that your time may run out.

2 – Fees for a fixed-rate mortgage could be too high

Lenders typically charge a fee in exchange for offering to fix their rates for a set period of time.

It is essentially because they are taking the risk themselves on the Bank of England (BoE) rate rising during the fixed-rate period, so some of this risk is passed onto their borrowers in the form of an up-front fee.

These up-front fees can often cloud judgement when comparing various mortgage options.

In some situations, rates would have to increase exponentially in the short term to warrant the cost of the up-front fee. This is especially relevant when the borrowing large sums compared to the property value.

Consider up-front fees and compare savings + fees for the period of time the mortgage will be fixed.

3 – Not all fixed-rate mortgages are rising

According to the Bank of England (BoE), in June 2010, fixed rate mortgages were still being set around the 3.7pc mark. Four years later in 2014, they we closer to 2.7pc. And in 2015, they fell to just below 2pc, which was the lowest reported by BoE.

In the recent months, rates by a handful of lenders have started to increase slightly.

However, as one lender increases their fixed rate another one is still dropping theirs, in an attempt to win business.

Even though there is much speculation around rates rising, the proof is in the pudding and there are still many cuts taking place every week.

4 – Variable rates may not rise even if the BoE rate does

Borrowers with a Tracker mortgage may still have a very competitive mortgage despite a BoE rate rise.

Those with a SVR mortgage may find a better deal by remortgaging, however another similar “variable” product may work better for them, depending on the level of debt, desire for commitment or flexibility and other factors.

5 – Your Tracker rate may be excellent

Some historical Tracker rates are too good to be true and can’t be found now. This is particularly true of some agreed in 2005 and 2006, before the crisis hit. Also, some borrowers with “lifetime” rates could be in the same boat.

It is typical that switching lenders can save money. However, like these example, there may be some situations.

Make sure any decision takes into account your personal circumstances.

Weighing everything up

However, take into account that a fixed rate offers less flexibility for moving property and fees are usually incurred unless you remain with the same lender and transfer your mortgage to a new property.

Instead of only basing decisions based on predictions of rate increases, that may or may not materialise, base your choice of mortgage base your decision on your attitude to risk as well as your short, medium and long term plans.