There are certainly advantages to longer term mortgages (anything with a term over 30 years). A homeowner usually ensures lower monthly payments spread out over a longer period, and changes to the Bank of England base rate will have little to no effect on their ability to borrow. Unfortunately, the downside is that they are more expensive overall and will take a borrower longer to pay off.

This article does not constitute advice. Professional advice should be taken prior to acting on any part of it. Your home may be repossessed if you do not keep up repayments on your mortgage or any other debt secured on it.

In recent years, it’s become increasingly popular for banks and building societies to offer more long-term mortgages – some even offering loans with repayment terms over 35 years. As mentioned, this might seem like a win-win for borrowers and providers alike, but experts warn it could be setting up massive headaches in the future. Borrowers may see these terms and jump at the chance for lower payments without weighing the risk of being locked into a mortgage for almost ten years longer than the traditional 25-year deals that have been prevalent for decades.

Rising house prices might make these longer-term deals seem appealing.

As your monthly payment will be lower, buying a house becomes a lot more affordable for a lot of people. But in reality, having longer terms would mean many borrowers would be repaying their mortgage for longer than normally anticipated and that could risk running into retirement.

The risks of this? It will certainly cut into prime saving years for retirement by putting money towards a mortgage instead of a pension when many individuals are in their peak earning years. Then there’s the additional interest that borrowers will be saddled with.

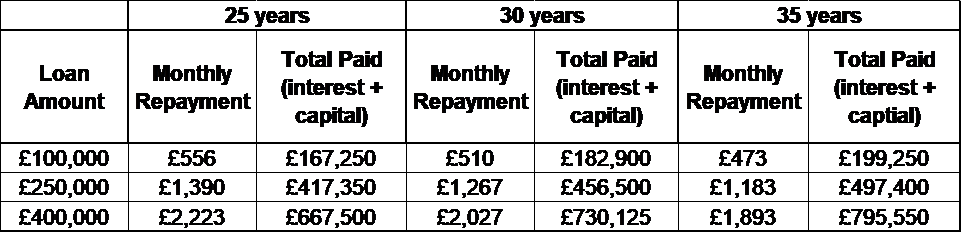

Let’s take a look at examples of small, medium, and large mortgages to see the true cost over 25, 30, and 35 years. For each, assume an upfront charge of £500 and an average interest rate of 4.5%.

As you can see, when comparing the total amount that would be repaid over the term of the loan, a ten-year gap could mean paying almost 20% more to your lender. For smaller loans, your monthly repayments don’t even change too much, but one could argue that in comparison you’re still not paying much less each month, and either way the maths just doesn’t add up.

If you’re in the market for a home and aren’t sure what kind of terms are right for you, get in touch with us today. We’re here to help you find your next home – and of course, at the right price.

Need help to secure a low-cost mortgage? Mortgages | Buy to Let | Property | Mortgage Planning |

Dental & Medical Financial Services have been helping doctors and dentists with finding low-cost mortgages for your home and investment properties for over 25 years. Call Chris to discuss your options. Tel: 01403 780 770

?

If you found this article interesting, why not share it

If you found this article interesting, why not share it

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful. You can adjust your preferences here. Please see our privacy policy for more information relating to GDPR.

All questions, comments and requests regarding this Cookies Policy should be addressed to [email protected] write to Us at 1 Market Square, Horsham, West Sussex, RH12 1EU.

Or alternatively please contact our Compliance Director at Best Practice IFA Group Ltd, Broadlands Business Campus, Langhurst Wood Rd, Horsham, RH12 4QP, telephone number 01403 334455, or via email at [email protected]

Strictly Necessary Cookies

These cookies are necessary for the website to function and cannot be switched off in our systems. They are usually only set in response to actions made by you which amount to a request for services, such as setting your privacy preferences, logging in or filling in forms. You can set your browser to block or alert you about these cookies, but some parts of the site may not work then.

Cookies used:

moove_gdpr_popup - Stores user preferences in regards to cookie settings

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.

3rd Party Cookies

This website uses Google Analytics and other marketing cookies to collect anonymous information such as the number of visitors to the site, and the most popular pages.

Keeping this cookie enabled helps us to improve our website.

Cookies used:

Google tag manager

Please enable Strictly Necessary Cookies first so that we can save your preferences!