Our 5-minute read – Tax Tips – for UK doctors and dentists will help you save tax, get organised with your tax affairs and make sure you meet important deadlines with ease.

This article does not constitute advice. Professional advice should be taken prior to acting on any part of it. The Financial Conduct Authority does not regulate tax advice.

Every time you wrap your head around all the ways you can save on your tax bill, rules get amended, allowances are changed, and you find yourself needing to relearn tax laws all over again. Don’t miss out on the relief you’re entitled to and make sure your hard-earned money stays in your pocket where it belongs.

What are the allowances?

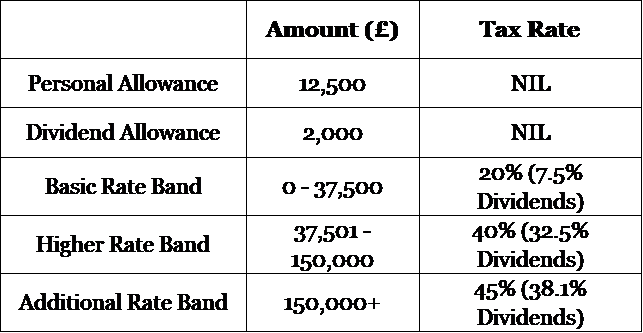

The start of the tax year is the best time to brush up on your knowledge and determine whether there is anything you can do to modify your personal income structure to take advantage of the available tax bands. Below we’ve highlighted the important tax tables you’ll live by for the 2019/20 tax year.

It’s no surprise that higher earning individuals are still being hit by the tapered personal allowance once their income surpasses the £100,000 threshold. In fact, anyone who makes £125,000 or more will lose their personal allowance completely as, for every £2 earned over the limit, the allowance is reduced by £1.

Unfortunately, earners within this tax brackets will be immensely impacted by the effective 60% rate of tax so now is the time to buckle down and uncover ways to save on tax.

Ways to save for company directors

Director’s salary – A fairly prominent method of tax planning is to administer a tax-efficient director’s salary. The newly determined most favourable salary is now £719/month – up from around £680 – £700 due to increases in National Insurance thresholds.

By setting this income, you will find yourself in a win-win situation: you are successfully using your personal allowance, earning enough to qualify for the state pension, present a tax-deductible expense for your company, and your earnings will fall below the National Insurance Contributions threshold, so your income won’t be taxed.

Draw dividends – Another way for company directors to save is to draw dividends instead of taking more salary. This is because dividends are subject to an initial rate of tax that is lower than you’d be hit with if you took a conventional salary, plus you gain a more flexible way to draw what you’ve earned and when you do so.

Start planning for the tax year now

Now’s the time to visit a financial professional to review your goals for both the year and long-term. They can help adjust your plan according to new tax rules and allowances so you can be confident in your tax efficiency for the current tax year.

?