If you own a limited company and you have money in your business account not earning any interest, think about investing those funds. If your money isn’t earning interest, then taking inflation into account, in a few years’ time you could actually have less money because cash will lose its purchasing power. Find out how to invest your limited company profits and grow your wealth instead.

This does not constitute advice and advice should be sought in all instances before acting on it.

Often, when a limited company becomes profitable, the business owner takes income plus dividends up to a tax-efficient threshold and then the retained profits just sit in their account.

You can’t use those funds without paying tax on it, nor would it be considered a business expense. So, it ends up sitting in an account, and depending on the inflation rate over the years, could potentially lose money. The higher the inflation rate, the less you can get for your money.

The downside of leaving your profits sitting in your bank account.

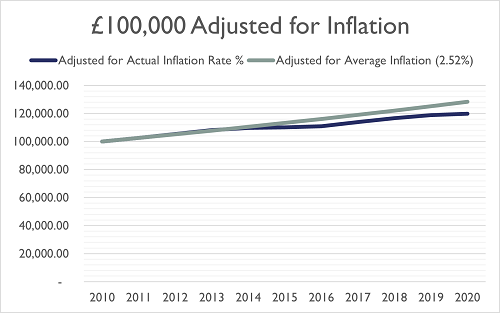

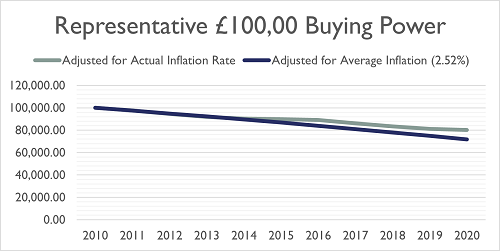

If you had £100,000 of surplus cash in 2010 and added on the UK yearly inflation rate, that is an additional £19,767 by the end of 2020.

So, if you don’t do anything with that £100,000 over the time period, and you take into account the UK inflation rate, your original £100,000 of buying power would be worth less. £100,000 becomes £80,232 of buying power. Or another way of looking at it is that £119,767 would now have the same buying power as your £100,000 did in 2010.

Almost £20,000 is a significant amount of money to lose.

Inflation rates sourced 11/06/2021

Investing through a limited company

If you wanted to take that money out you would have to pay 32.5%/38% dividend tax upfront. The trade-off is that you could put it into ISAs and other allowances. But keeping that money invested through the company and accessing it as little as possible could be a much more profitable strategy, long-term.

There are two ways you can invest though your limited company:

- Option 1: A holding company owns your trading company and receives the cash surplus as dividends.

- Option 2: You open a totally separate company and receive the money as a loan from trading company.

Most tax advisers agree that, having 2 companies as separate entities is a clearer structure and easier to set up.

If you invest via another limited company the trading company has better chances of qualifying for Entrepreneur’s Relief if the loan is repaid in full; Entrepreneur’s relief means that, should you plan to close down or sell your business you’ll only pay 10% capital gains tax on the gains.

It’s an important topic so it’s essential to seek advice on your personal or company investments.

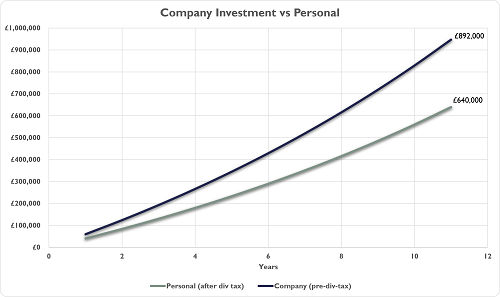

To demonstrate the point, let’s look at an example of what you could achieve if you invest through your limited company compared with personal investment.

If you invested £60k cash of profit each year, after 10 years, you could turn that into £892,000. This is assuming an average of a 7% annual return with corporation tax remaining at 19%.

In comparison, personally investing your £60k could see you achieve £640,000 over the same time period. That is a difference of £252,000.

After 10 years, you could choose to withdraw all or some of the money minus relevant taxes. This could be a much more profitable long term strategy for you.

Where to invest your funds

The strategy you should employ for investing through your company should be the same one you employ with your personal wealth. A diversified portfolio is important no matter whose money you’re investing — your company’s or your own. It’s the best way to ensure you can weather the storm in any one area of the market because you’ve got investments across the board.

In general, there are few things to consider when making your decisions. It might come down to which investment platforms are best for you so you can easily track your investments and tax liabilities. Think about where you want to be in 5 to 10 years and what other long-term savings and investments plans you have like pension pots or property and what would be the best mix for your particular situation.

Work with a professional

Investing through a limited company no matter which way you choose to invest will undoubtedly have some tax implications. A financial adviser could help you decide which strategy is right for you.

At Dental & Medical Financial Services we’re passionate about saving you tax and incorporating your tax affairs into your overall financial strategy. Get in touch with us today if you’re ready to ensure your wealth grows and is protected for years to come.

Can your money work harder for you?

Can your money work harder for you?

Investments | Financial Planning | Retirement | Save Tax | Protection |

Can your money work harder for you?

Can your money work harder for you?Dental & Medical Financial Services have been helping doctors and dentists to build and protect their wealth, whilst saving tax for over 25 years.

Tel: 01403 780 770

?