This information is based on Conservative Manifesto and election pledges. There is no guarantee this change to pension tax relief for high earners will take place. Information is based on the details available. For advice, you need to speak to an Independent Financial Adviser.

How pension tax relief is calculated now

The current pension system allows everyone to claim back 20% from the Government as tax relief on pension contributions made within the year. For example, a contribution of £8,000 is topped up by an additional 20%, so £2,000, by the Government, leaving a £10,000 overall addition to your pension.

Even non tax-payers can claim some tax relief back, including children.

Read more: Tax relief on pension contributions – claim your share

Higher-rate and top-rate tax payers can claim back more, 40% and 45% respectively. For example, a higher rate tax payer would need to contribute £6,000 to effectively achieve a £10,000 pension contribution, with the Government adding £4,000 (40%). For top-rate tax payers it would be a cost of £5,500 (45%) with a contribution from the Government of £4,500.

Subsequently, making pension contributions is a popular tax efficient strategy for retirement planning, used by many doctors and dentists where their income falls outside of basic rate tax.

What pension tax relief cuts are possible?

The Conservatives currently spend over £34 million a year in total on pension tax relief. This policy is in place to encourage pension savings, however, their intention would be to cut tax relief for those earning over £150,000 from salaries and bonuses from UK employment, including directorship.

Currently, tax relief can be claimed up to the level of tax that is paid above basic rate. There is an annual allowance cap though at £40,000 for pension contributions.

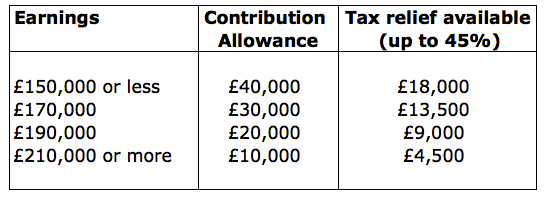

The Conservatives proposal is that for every £2 earned above £150,000, the annual allowance would be cut by £1. This could effectively mean that tax relief on a £40,000 contribution, for someone earning over £210,000, could be as little as £4,500, compared to current tax relief, which would be a maximum of £18,000. This is because the allowance would be reduced to £10,000 from the proposed cuts.

How tax relief could be reduced for higher earners:

Proposed cuts, if they come to fruition, may take place immediately or they may take place at a future date. There is no indication at the moment.

What action can be taken now?

If you earn over £150,000 and want to take precautions in advance of Wednesday 8th’s Second Budget announcement, you should speak immediately to a Financial Adviser who can help explain your options.

Options could include:

- Bringing forward contributions for this year to ensure you maximise the tax relief available – particularly if you have money in the bank and were planning to contribute a lump sum this year anyway.

- Consider using any unused allowances from the previous three years. The allowances were £50,000 for 12/13 and 13/14 and then £40,000 for 14/15 and can be utilised as long as you had a pension scheme running during those years. Other terms may apply.

Points to note:

- The value of pension investments can fall as well as rise so you may get back less than you invest

- Personal pensions can usually only be accessed after age 55, or 57 from 2028

- The full pension can be withdrawn, but only 25% will be tax free. Remember also, your pension needs to last you through retirement unless you have other income sources.