Nearly three-quarters (73%) of financial advisors have reported to Prudential Research firm that their clients have been impacted by the introduction of the tapered annual allowance. In fact, in the first year it was introduced, reports of annual allowance breaches doubled – that’s a lot of people who could have benefitted from a little help.

This does not constitute advice and advice should be sought in all instances before acting on it. The Financial Conduct Authority does not regulate tax advice.

The tapered annual allowance has been a hot topic for a while in the financial planning world – and for good reason.

Ever since its introduction in April 2016, the tapered annual allowance has been a thorn in the side of the healthcare industry as many doctors and dentists do reach the level of income affected by the tax law.

The reduced annual allowance targets individuals with an adjusted income (all taxable income and pension savings minus certain tax reliefs) of over £150,000. This means that for every £2 over £150,000 an individual makes, their allowance is reduced by £1, with a minimum annual allowance set at £10,000.

However, if your threshold income (income less employer pension contributions) is no more than £110,000, your income will not be subject to the tapered annual allowance.

Is it really that simple?

Sounds simple enough, in theory, but unfortunately, the calculations involved to get the baseline numbers in which the assessment on your allowance is made are quite complicated. So, if you find yourself in need of assistance – which is likely as the calculations for adjusted income and threshold income are highly involved – you should speak to a professional.

Looking specifically at the healthcare sector, the impact has been vast. Doctors and dentists are more likely to be subject to an annual tax charge on contributions and a lifetime allowance tax charge on their benefits and concern over their pensions is increasing.

Nine out of ten doctors who have previously breached the annual allowance have either already sought professional financial advice or plan to do so.

Out of 2,500 doctors involved in the NHS Pension Scheme surveyed by pension provider First Actuarial, 67% reported that they plan to seek professional tax help or will take advice from an advisor.

Seeking out the right professional help

Doctors and dentists might find it difficult to secure an Independent Financial advisor well versed in the topics necessary to help them navigate the potential minefield of tax issues that might be coming their way should they be affected by the tax legislation.

Do not fear. Dental & Medical Financial Services are specialists with knowledge and experience of dealing with NHS pension schemes, the complexities around the threshold and adjusted income, pension, growth values, carry forward and tapering allowance calculations. And as part of our service to clients, we provide carry forward and tapering pension allowance calculations at no extra cost.

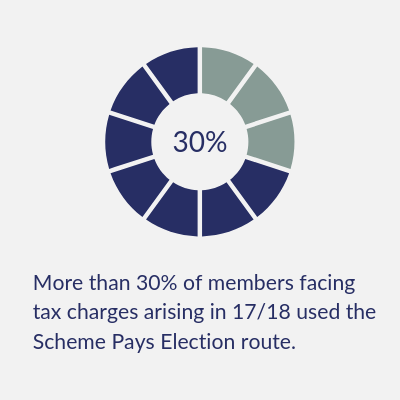

Time is running out to use Scheme Pays

The outcomes of these calculations will determine if there is an excess tax charge, and the options available to the member in settling any tax charges, whether that is via the NHS scheme pays route or via self-assessment.

More than 30% of those members facing tax charges arising from 2017/18 elect to use the scheme pays route and the deadline for scheme pays election is July 31st, 2019.

So, don’t delay – get in touch with us today.

Need help to reduce your tax burden? Investments | Financial Planning | Retirement | Save Tax | Protection |

Dental & Medical Financial Services have been helping doctors and dentists to build and protect their wealth, whilst saving tax for over 25 years.

Tel: 01403 780 770

?

If you found this article interesting, why not share it

If you found this article interesting, why not share it

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful. You can adjust your preferences here. Please see our privacy policy for more information relating to GDPR.

All questions, comments and requests regarding this Cookies Policy should be addressed to [email protected] write to Us at 1 Market Square, Horsham, West Sussex, RH12 1EU.

Or alternatively please contact our Compliance Director at Best Practice IFA Group Ltd, Broadlands Business Campus, Langhurst Wood Rd, Horsham, RH12 4QP, telephone number 01403 334455, or via email at [email protected]

Strictly Necessary Cookies

These cookies are necessary for the website to function and cannot be switched off in our systems. They are usually only set in response to actions made by you which amount to a request for services, such as setting your privacy preferences, logging in or filling in forms. You can set your browser to block or alert you about these cookies, but some parts of the site may not work then.

Cookies used:

moove_gdpr_popup - Stores user preferences in regards to cookie settings

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.

3rd Party Cookies

This website uses Google Analytics and other marketing cookies to collect anonymous information such as the number of visitors to the site, and the most popular pages.

Keeping this cookie enabled helps us to improve our website.

Cookies used:

Google tag manager

Please enable Strictly Necessary Cookies first so that we can save your preferences!

Need help to reduce your tax burden?

Need help to reduce your tax burden? Need help to reduce your tax burden?

Need help to reduce your tax burden?